Cash Management Software to Manage Your Entire Cash Ecosystem

Tap into the power of automated cash management today. Replace your fragmented systems with a unified cash management platform that gives you all the control you need without the complexity.

Improve Operations with Sonas’ Automated Cash Management

These are our independent products, powerful tools that together form a complete cash management solution. They can be adopted separately or together to meet any business requirement and deliver real-time control with measurable ROI.

Order Management

A unified system for creating and tracking all cash orders. Create, track, and automate orders with real-time visibility for teams, clients, and partners.

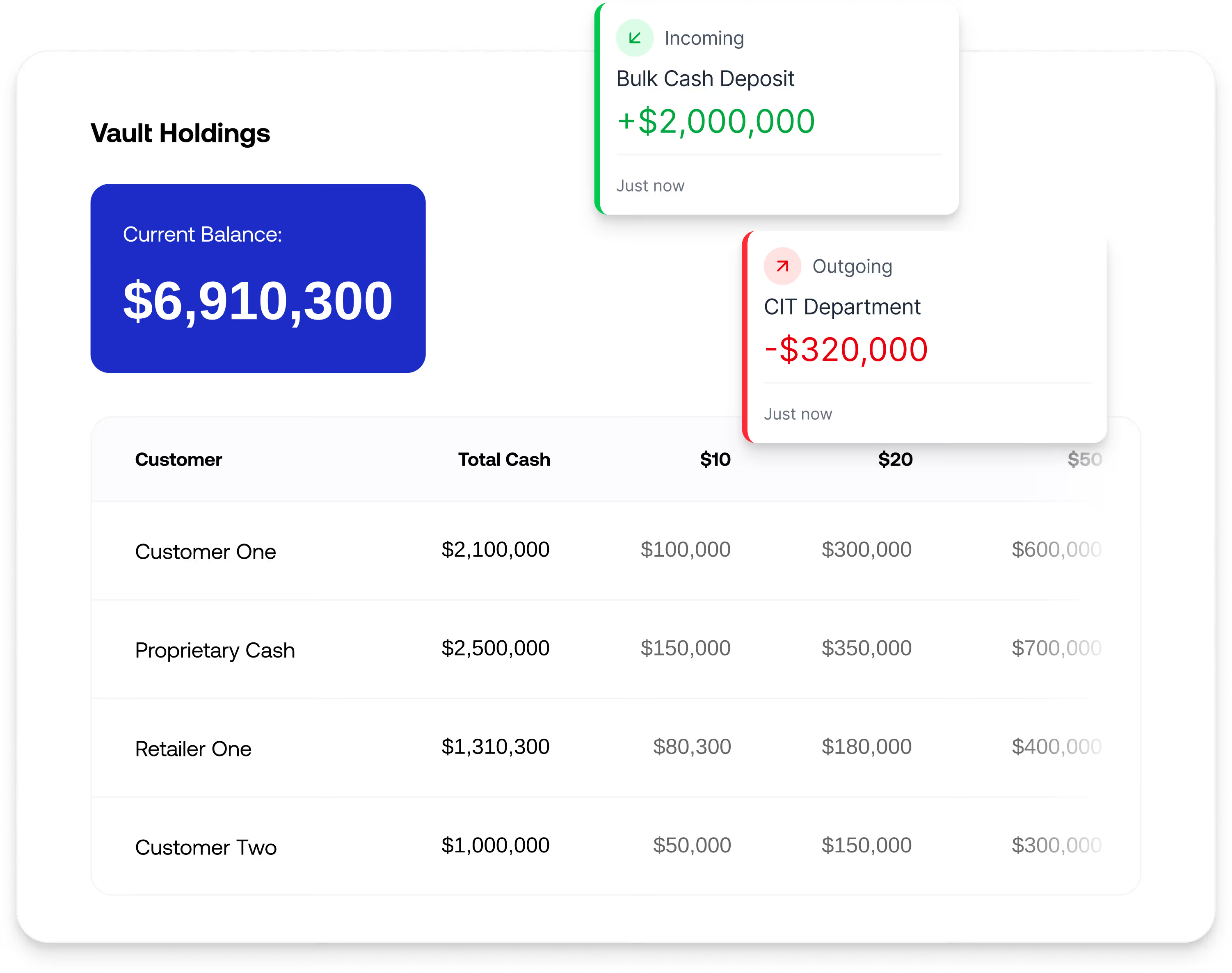

Vault Balancing & Cash Processing

Record cash movements, manage workstation processing, and monitor live vault holdings with full auditability and client visibility.

Track & Trace

Gain scan-by-scan visibility into every cash movement. Eliminate losses with a real-time digital chain of custody from vault to destination.

Intelligent Route Management

Dynamically generate and update routes. Slash planning time, reduce fuel costs, and boost fleet efficiency.

Cash Forecasting

Forecasting cash demand with precision. Use historical data and event trends to optimise inventory, prevent cash-outs, and free up capital.

Automated Cash Reconciliation

Automatically match ATM, bank, and CIT data. Eliminate manual spreadsheets and achieve 100% accurate, instant reconciliation.

Transactional Reconciliation Engine

Our most powerful reconciliation tool. A rules-based engine to automate the matching of any dataset, regardless of source or complexity.

Unified Case Management

Your central hub for all exceptions and claims. Streamline investigations and resolutions on a single, collaborative, auditable platform.

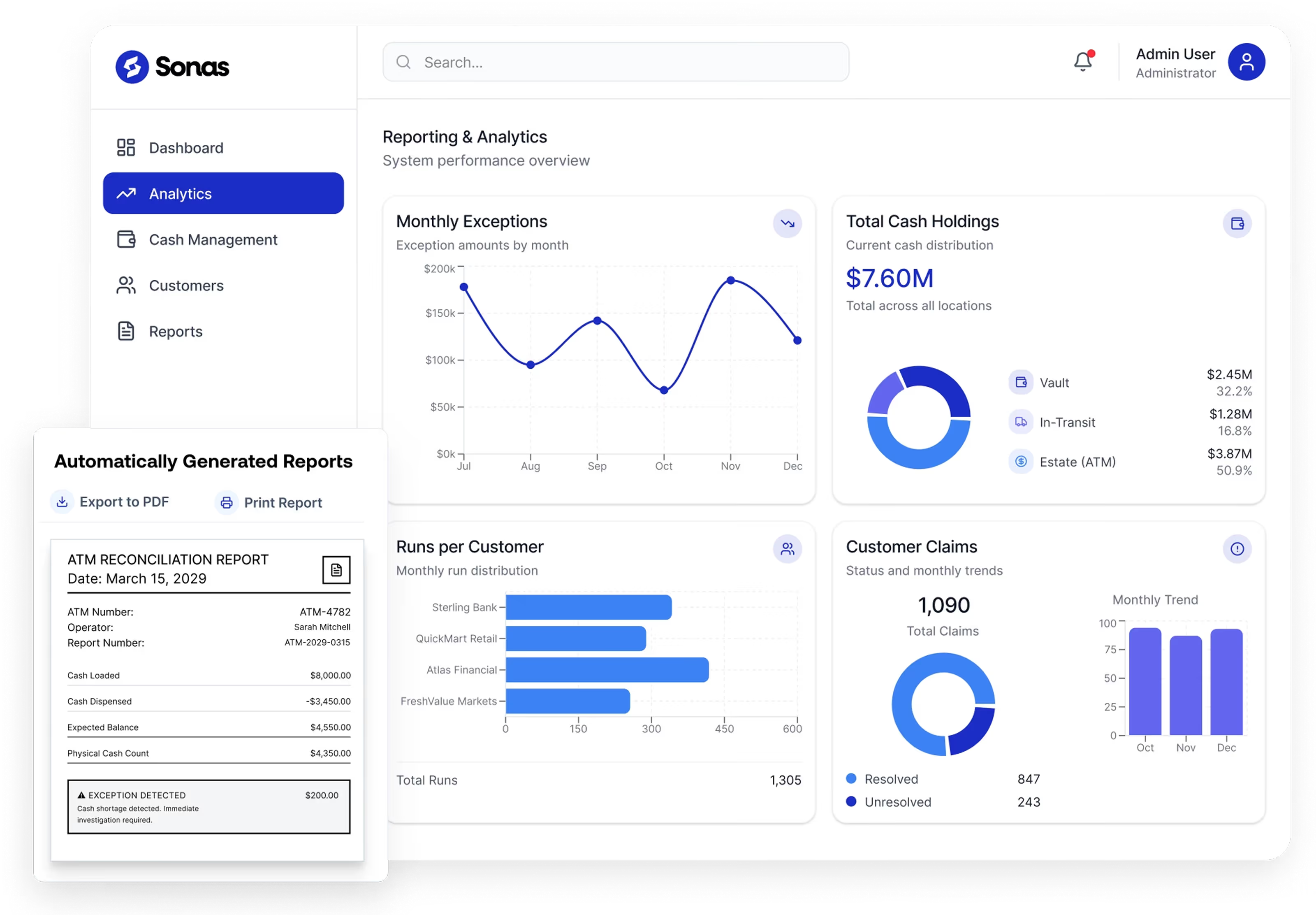

Intelligence & Analytics Hub

Turn operational data into actionable insights. Sonas customisable dashboards and deep-dive reports for data-driven decision-making.

Drive Meaningful Change

Hours Saved Per Week in Reconciliation

%

Improvement in Cash Utilisation

X

Faster Dispute Resolution

%

Vault Balance Accuracy

Sonas Cash Management Platform Connects Your Entire Cash Ecosystem

See how our unified cash management software supports visibility, control and efficiency across different industries.

Unify vaults, routes, tracking, and reconciliation. Reduce costs, prevent losses, and improve service delivery.

Automate forecasting, prevent cash-outs, and reconcile your network through Sonas platform for maximum efficiency.

Reconcile ATM transactions instantly, optimise cash, and gain complete visibility across your network.

Monitor kiosk cash levels, automate reconciliation, and streamline crypto cash operations across your network.

Match transactions to bank files, streamline disputes, and ensure accurate settlements with every partner.

See Everything. Automate Anything. Lose Nothing.

One unified platform for your entire operations.

Eliminate spreadsheets.

Reconcile thousands of transactions instantly.

Gain real-time visibility into all cash movements.

Prevent cash-outs and free up capital.

Cash Operations,

On the Go

Manage routes, track cash, and record operations—all from a single mobile app.

Digital record of all field operations in real-time

Scan barcodes with Track & Trace for complete visibility.

Route Management integration lets drivers view their stops.

One Cash Management System To View Your Entire Operations

See how our solution brings siloed data and physical workflows into a single, automated command centre

Hear How We Transform Cash Operations

Unify your entire operation—from vault management and route optimization to real-time tracking and automated reconciliation. Slash costs, eliminate losses, and transform your service delivery.

Managing my finances has never been easier. Their expert guidance and tailored strategies have transformed my approach to cash flow, making it more efficient and profitable. Managing my finances has never been easier. Their expert guidance and tailored strategies have transformed my approach to cash flow, making it more efficient and profitable.

Cameron Williamson

Crypto ATM Operator

Managing my finances has never been easier. Their expert guidance and tailored strategies have transformed my approach to cash flow, making it more efficient and profitable. Managing my finances has never been easier. Their expert guidance and tailored strategies have transformed my approach to cash flow, making it more efficient and profitable.

Cameron Williamson

Crypto ATM Operator

Managing my finances has never been easier. Their expert guidance and tailored strategies have transformed my approach to cash flow, making it more efficient and profitable. Managing my finances has never been easier. Their expert guidance and tailored strategies have transformed my approach to cash flow, making it more efficient and profitable.

Cameron Williamson

Crypto ATM Operator

Explore Industry-Specific Solutions from Sonas

Access our product brochures to learn how we can simplify and automate your operations.

.avif)

Automation that modern cash management organisations need to operate efficiently and profitably.

.avif)

Flexible cash management software for banks and credit unions, supporting accuracy, compliance, and smarter decision-making.

.avif)

IAD software that supports in-house operations, outsourced partners, and everything in between.

.avif)

Automated settlement reconciliation and simplified, reliable reconciliation across your network.

.avif)

Crypto ATM software, to streamline cash handling, settlement, reconciliation, and crypto transaction monitoring.

News and Industry Insights

Get latest insights, tips, and tricks on how automated cash management helps your business and enhance your operations.